Wednesday 9 June 2021

Tuesday 22 September 2020

IPO – Process, How to buy Shares, Risks and Returns

An IPO or Initial Public Offering is the process for private companies to go public by selling and making their stocks available to the general public. This is done by getting listed on an exchange. The process of an IPO is open to all companies new and old.

1. Introduction

With the help of an IPO, companies are able to raise equity capital by issuing shares to the general public. This can also be done by selling off the shares of the existing shareholders without raising any new capital. A company that offers shares to the public is in no way obligated to repay the capital to the investors (public). The company offering its shares is referred to as the issuer. The issuing of shares is done with the help of investment banks. Once the IPO is done, the shares of the company are traded in the open market. These shares can then be further sold by investors through tradings in the secondary market.

2. What is the need for an IPO?

IPO is an avenue through which companies can access capital and grow. The main objective of an IPO is to raise money by borrowing through the issuing of shares to the public. This is known as the first public invitation in the stock markets and hence the name IPO. Buying these shares allows the investor an ownership in the company in accordance with the value of the shares owned.

3. The process of an IPO in India

a. In India, it is the Securities and Exchange Board (SEBI) that regulates the process of an IPO and companies hoping to issue shares through an IPO have to first register with SEBI

b. A company must submit the necessary documents with the SEBI which then is analysed and is approved only when the SEBI is convinced

c. While SEBI evaluates the application, the company is required to prepare its prospectus, stating that the approval from SEBI is pending

d. On getting the approval from SEBI, the company is required to determine the share price of the shares to be issued and disclose the number of shares it plans to issue

e. The company must decide between the two types of IPO issues

i. Fixed Price IPO is one where the company decides in advance the price of the shares

ii. Book Building IPO is where the company provides a range of prices and there is a bid for shares within that price range

f. The shares are made public once the company decides the type of IPO they want to go with. The interested investors submit their applications and once the company receives the subscriptions from the public, it allots the shares

g. The company now lists the shares on the stock market and post the issuance in the primary market, it gets listed in the secondary market. These are then open for trading on a daily business.

4. How to Buy Shares from an IPO?

Step 1: You may acquire the physical application form from a broker or a distributor or a bank branch. The same can be accessed online

Step 2: You can then fill the form with your details, both personal and bank and demat account related

Step 3: Provide your total investment amount

Step 4: The shares will be allotted within 10 days from the date of closing (of the offer)

5. Important considerations before an IPO subscription

It is important to know of the market dynamic before investing in shares. Read the prospectus issued by the company and go throughout the financial details. These will shed light on the amount of money the company intends to raise and the types of shares they plan to issue. It is wise to also understand how the company plans to use the money raised from the IPO and its expansion plans. All these will help an investor make an informed decision.

6. The Risk and Reward

When you subscribe to a share during an IPO, you become one of the first shareholders of the company. As the company flourishes, the share price will rise and you will stand to profit. But there is also the risk of the stock markets. The returns on your investment will depend on the growth potential of the company and if the company fails, you will risk losing your money. Particularly in the case of unlisted companies, one has to be very careful as these companies are not required to publish their financials and thus, you can’t analyze their past performance.

IPO investments carry the risk of market fluctuations and must be undertaken after careful consideration. If you are unsure about investing, visit ClearTax where we have a list of handpicked investment options for you to pick from.

Tuesday 18 August 2020

SFT – Statement of Financial Transaction

Tax Reforms 2020 : 13/08/2020

The scope of Statement of Financial Transactions (SFT) has been expanded to widen the tax base. Once the CBDT releases the notification in this regard, the notified persons should report the following transactions in their SFT:

- Payment to hotels above Rs. 20,000

- Payment of property tax above Rs.20,000

- Payment of health insurance premium above Rs.20,000

- Payment of rent above Rs.40,000

- Payment of life insurance premium above Rs.50,000

- Electricity consumption above Rs.1 lakh

- Payment of educational fee/donations above Rs.1 lakh p.a

- Purchase of jewellery, white goods, painting, marble etc. above Rs.1 lakh

- Deposit/credits in the current account above Rs.50 lakh

- Deposit/credits in the non-current account such as savings accounts above Rs.25 lakh

- Domestic business class air travel or foreign travel

- Share transactions/D-MAT accounts/Bank lockers

Also, it is to be noted that the following persons should file their SFT return mandatorily:

- A person having bank transactions above Rs.30 lakhs

- All professionals and business having turnover above Rs 50 lakhs

Saturday 12 January 2019

32nd GST Council meeting

32nd GST Council meeting was held at New Delhi and chaired by Shri Arun Jaitley. Announcements made was a big relief to MSMEs and small traders.

- Increase in GST registration limit from Rs 20 lakhs up to Rs 40 lakhs for suppliers of goods.

- Changes in the existing composition scheme made by increasing the turnover limit to join the scheme up to Rs 1.5 crores, tax payments to be made quarterly and returns to be filed annually starting 1st April 2019.

- New composition scheme is introduced for service providers and those who supply services along with goods; the Turnover limit set is Rs 50 lakhs and the Tax rate is fixed at 6%.

- No rate cuts were announced this time. GoMs were formed to study taxation of under-construction properties & lotteries.

- Calamity cess up to 1% for up to 2 years will be charged for supplies made within the State of Kerala.

Wednesday 9 January 2019

GST State Code List

GST State Code List of India

| State code list under GST | State | State code list under GST | State |

|---|---|---|---|

| 01 | Jammu & Kashmir | 19 | West Bengal |

| 02 | Himachal Pradesh | 20 | Jharkhand |

| 03 | Punjab | 21 | Orissa |

| 04 | Chandigarh | 22 | Chhattisgarh |

| 05 | Uttarakhand | 23 | Madhya Pradesh |

| 06 | Haryana | 24 | Gujarat |

| 07 | Delhi | 25 | Daman & Diu |

| 08 | Rajasthan | 26 | Dadra & Nagar Haveli |

| 09 | Uttar Pradesh | 27 | Maharashtra |

| 10 | Bihar | 28 | Andhra Pradesh |

| 11 | Sikkim | 29 | Karnataka |

| 12 | Arunachal Pradesh | 30 | Goa |

| 13 | Nagaland | 31 | Lakshadweep |

| 14 | Manipur | 32 | Kerala |

| 15 | Mizoram | 33 | Tamil Nadu |

| 16 | Tripura | 34 | Puducherry |

| 17 | Meghalaya | 35 | Andaman & Nicobar Islands |

| 18 | Assam | 36 | Telengana |

| 37 | Andrapradesh(New) |

Saturday 29 September 2018

CBDT Extends ITR and Tax Audit Report filing due date for AY 2018-19 to 15.10.2018

F.No. 225/358/2018/ITA.II

Ministry of Finance

Department of Revenue

Central Board of Direct Taxes North-Block, ITA.II Division

Order under Section 119 of the Income-tax Act. 1961

Under Secretary to the Government of India

- PS to F.M./OSD to FM/PS to MoS(R)/OSD to MoS(R)

- PPS to Secretary (Finance)/(Revenue)

- Chairperson (CBDT),All Members,Central Board of Direct Taxes

- All CCsiT/CCsiT/Pr. DsGIT/DsGIT

- All Joint Secretaries/CsIT, CBDT

- Directors/Deputy Secretaries/Under Secretaries of Central Board of Direct Taxes

- ADG(Systems )-4 with request to place the order on official website

- AddI. CIT,Data base Cell for placing the order on irs officers website

- The Institute of Chartered Accountants of India,IP Estate, New Delhi-110003

- CIT (M&TP),CBDT with request to issue appropriate Press-Release and for placing on Twitter handle of the department

Thursday 20 September 2018

TCS and TDS applicable from 1st Oct'18 as per GST Law

| TCS and TDS applicable from 1st Oct'18 | ||||

| After putting it off for long, CBEC finally made TDS and TCS applicable from 1st October 2018. Let's understand these briefly. TCS must be collected by every e-commerce operator if this operator collects payment on behalf of a seller. Rate should not exceed 2% (exact rate will be notified in due course). Such TCS collected must be deposited to the govt within 10 days after the end of the month in which it was collected. TDS must be deducted where total value of supply exceeds Rs 2.5L. This only applies where the payer is a government entity (central and state govts, local authority, govt agency) or those notified by the govt as GST Council may suggest from time to time. Implications - TCS will add another layer to your reconciliation process for GST. As a seller on an e-commerce website, your outward supplies must match those reported by the operator. If these don’t match, you’ll have to add them to your outward supplies and pay relevant tax and interest on them. Reconciling with your operator becomes critical to make sure you face no additional tax liabilities while filing your return. As an e-commerce operator, you will have to start filing GSTR-8 to start reporting your TCS collections and also reconcile with sellers on an ongoing basis.

|

Tuesday 18 September 2018

What is the last date to claim Input Tax Credit under GST for FY 2017-18 ?

What is the last date to claim Input Tax Credit under GST for FY 2017-18 ?

- after the due date of furnishing of the return under section 39 for the month of September following the end of financial year to which such invoice or invoice relating to such debit note pertains or

- furnishing of the relevant annual return,whichever is earlier.

Wednesday 29 August 2018

ITR filing deadline extended to 15th September for Kerala assessees

|

Digital Signature Certificate @ just Rs 799click on the nameINDIAN DSC SERVICES |

Highlights

- Last date for filing ITR has been extended to 15.09.2018 for all income tax assessees in Kerala for whom the deadline till now was August 31, 2018

- Extension given as a relief measure due to severe floods in the state. This year penalty is leviable on late returns

Due to disruption caused by severe floods in Kerala, the Central Board of Direct Taxes (CBDT) has extended the due date for filing income tax returns (ITR) for all income tax assessees in Kerala to September 15, 2018, as per an official release here today.

Until last assessment year (AY) there was no penalty for filing belated income tax returns. However, this penalty is applicable from FY 2017-18 or AY 2018-19. A new section 234F was inserted by the go .

Clearly, the deadline for ITR filing for Kerala residents has been extended as a relief measure for the state's residents who are already battling nature's fury.

Thursday 16 August 2018

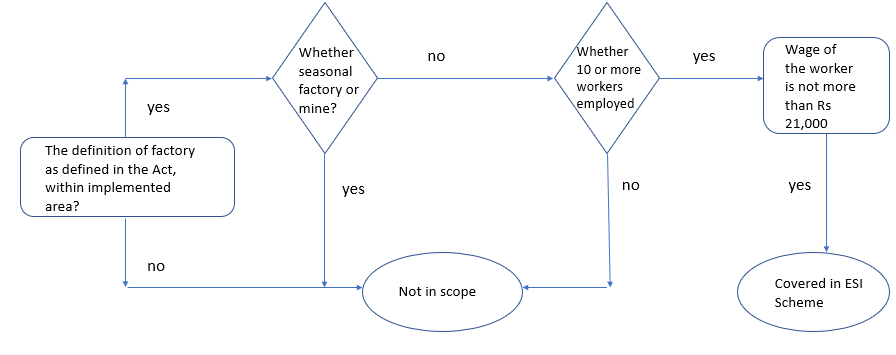

ESIC and its applicability

Applicability of the ESI scheme

Features of the scheme

Friday 27 July 2018

Income Tax Return Filing Deadline Extended By A Month To August 31

Assessees can now file their income tax return (ITR) for assessment year 2018-19 (financial year 2017-18) by August 31 without any penalty charges.

Wednesday 25 July 2018

JSON file errors and Possible suggestions/Actions to be taken…

| 1 | Jason file uploaded successfully with no error report but less invoices updated on GST portal Suggestion/Action to be taken 1. Values accepted only up to 2 decimal point. More than 2 decimal figures will not be updated on online portal. Round up values in this manner only

2. Cross tally total invoice numbers uploaded and reflected in online portal

3. This error is due to wrong GST number of customer in Jason file

4. Cross tally for total turnover details and aggregate turnover details as same is not reflected when Jason file is uploaded.

Q2 : GST number is not correct

Utmost care must be taken while uploading the details in offline tool for GST numbers. It should be always validated well from GST portal

Q3 : Error in Json structure validation

1. Punching of state name instead of selecting from dropdown in excel utility

2. Multiple tax rate in one invoice but same has punched with single line

3. Wrong Port code or Shipping bill number

4. In case of exports without payment of duty – selecting GST rate other than 0%

5. No special character should be present in any cell

i. Ensure that GSTIN is mentioned in the JSON file.

ii. Ensure that you have uploaded the most recent and correct JSON file in the GST Portal under the correct GSTIN.

iii. If the problem still persists, download the latest version of the GST Offline return tool or GST software and prepare the JSON file

Q 4 :No Gross turnover details reflecting after uploading JSON file

Cross tally for total turnover details and aggregate turnover details as same is not reflected when Jason file is uploaded. You are required to punch the same online and save the same.

Q5 : No documents issued reflected in Table no. 13

Cross tally for document issued during the period details (Table no.13) as same is not reflected when Jason file is uploaded. You have to update and save and wait for some time to update the same

Q6 : No section data or Gross Turnover is available to process the request

If you’re filing a NIL return without any invoices, you need to punch in table no.8 all values to 0 (again) then save the return. Error will be resolved

Q7 : The GSTIN is invalid. Please provide a valid GSTIN

1. Download JSON report and open in Word Doc

2. Search for the error number‘RET191113’

3. You will see the invoices where the issue has occurred.

4. Note the invoice numbers

5. Correct the GSTIN and then re-upload to GSTN portal

Q8 :The rate entered is not valid according to the Rate List

You must have not entered correct tax rates. Kindly round off the tax rate before uploading the same in excel utility or CSV file.

Q9: Invoice number does not exist. Please enter a valid Invoice number.

Invoice Number should be alphanumeric, a maximum of 16 characters in length, and can contain only ‘-’ or ‘/’ as special characters. Please check that all invoice numbers follow this format.

Q10 : Invoice already exist with different CTIN or same CTIN. Please delete the existing invoice and re-upload again

1. Check if the invoice is already uploaded on govt portal:

2. Ignore the error if the invoice is uploaded and you don’t need to make any changes

3. To make changes, delete the old invoice on the government portal.

4. Upload the changed invoice with proper JSON file

Q11: Date is Invalid. Date of invoice cannot be before registration date.

1. This is possible that invoice date you have mentioned is earlier than the date on which your customer has obtained their GSTIN registration.

2. Delete the these invoices

3. Enter these invoices to B2C(S) section

4. Your client may not be eligible for ITC in such cases

|